The benefits when using credit scores

Granting Credit

Credit does not come for free and it involves risk. To mitigate such risk and to ensure prompt payments, creditors, banks and financial institutions should consistently seek to protect their cashflow and profit. To assist suppliers selling on credit, MCB provides credit scoring reports to facilitate their creditworthiness analysis, hence enabling them to collect their dues on time.

What is a credit score?

A credit score is a snapshot of a customer’s creditworthiness and the ability to meet the repayment terms offered by the creditor, based on financial data and payment history of the customer.

A credit score provided by MCB, being an independent provider, is an effective tool a creditor would look at when analysing a credit application. The MCB credit scoring reports assist creditors to mitigate credit risk during their credit risk analysis.

Consent

MCB will issue a credit score, showing the level of creditworthiness of a customer, only with the customer’s prior consent.

How we can help businesses and sole traders selling on credit

It is of course essential to carry out a credit risk assessment when onboarding new customers, to whom credit terms are being offered. It is also necessary to monitor the creditworthiness of existing credit customers.

This is where MCB, Malta’s reputable credit reference agency, can help.

The credit report service offered by MCB allows creditors to assess the creditworthiness of an individual or company, using data sourced from local banks and found in the Central Credit Register at the Central Bank of Malta. This report provides you with the information required to assess the payment behaviour of prospective customers and their ability to meet their financial obligations when due.

How your credit score is calculated

MCB generates credit scores using information held at CBM’s Central Credit Register (CCR). It is the result of a statistical model that links success in making credit payments to aspects of your past credit history.

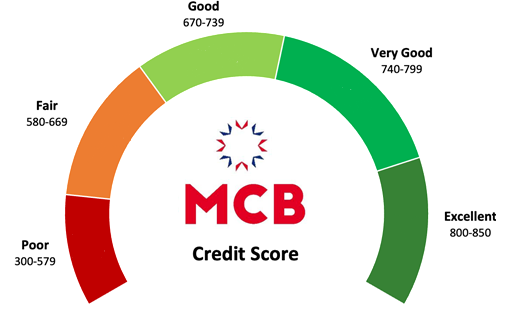

The MCB Credit Score is a three-digit number, ranging from 300 to 850. This score would reflect a collective summary of a consumer’s credit history and standing at that point in time.

A credit score is measured by taking into account factors such as:

- The length of time the creditor has benefited from the credit terms. The track record of this creditor would signal how responsible it has acted over the years.

- A creditor’s available credit compared to the credit used. Creditors may feel uncomfortable if the prospective new customer has already used a large percentage of available credit.

- The payment history, which shows whether the new customer has a history of paying credit obligations on time. A good track record, where payments are made on time, provides comfort to creditors.

- The number and type of credit accounts a customer has. Creditors prefer to see that a new client using a good mix of different types of credit responsibly and reliably.

- The number of new accounts a creditor has opened. This throws light on a customer’s ability to repay.

Interpreting credit score results

The higher the MCB Credit Score, the lower the risk to the creditor to offer credit to its customer.

A credit score will be a number in the range of 300 to 850 and will be interpreted as shown hereunder.

| CREDIT RATING | RISK LEVEL | Score Range | Description |

| Excellent | Very Low Risk | 800-850 | An exceptional borrower with extremely low credit risk and exceptional credit quality |

| Very Good | Low Risk | 740-799 | A very reliable borrower with low credit risk and very good credit quality |

| Good | Medium Risk | 670-739 | An average borrower with average credit risk and good credit quality |

| Fair | Medium to High Risk | 580-669 | A moderately risky borrower with average credit risk and moderate credit quality |

| Poor | High Risk | 300-579 | A risky borrower with high credit risk and low credit quality |